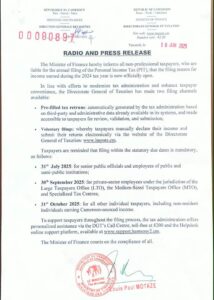

-

What is personal income tax?

Personal income tax is a levy on the total amount of annual income actually disposed of by a natural person in a year.

-

What is the scope of the PIT?

The scope of the PIT corresponds to all income that meets the conditions laid down by law for being subject to this tax.

In accordance with the provisions of Article 24 of the General Tax Code, the PIT applies to the following categories of income:

- salaries, wages, pensions and annuities;

- income from movable capital;

- property income;

- craft, industrial and commercial profits;

- agricultural profits;

- the benefits of non-commercial professions;

- non-commercial income.

-

Who is taxable at the PIT?

A taxable person is a person who falls within the scope of the tax.

Pursuant to the provisions of Article 25 of the General Tax Code, subject to international tax treaties, all natural persons having a tax domicile in Cameroon are taxable to the PIT.

-

What are the criteria for tax domiciliation in Cameroon?

Persons deemed to be resident for tax purposes in Cameroon are those who:

- have their home or principal place of stay in Cameroon;

- engage in an occupation in Cameroon, whether employed or not, unless that occupation is pursued there as an ancillary activity;

- They have the centre of their economic interests there.

The following are also considered to be tax residents in Cameroon:

- government officials or agents posted abroad not taxed locally;

- persons, resident or not, receiving income from Cameroonian sources;

- persons whose income is taxable in Cameroon under a tax treaty;

- locally recruited staff from diplomatic missions, consular posts or international organisations.

-

What income must be declared by a Cameroonian tax resident?

Every resident for tax purposes in Cameroon is required to declare all his global income, whether from Cameroonian or foreign sources, in accordance with the principle of globality provided for in Article 25 of the General Tax Code.

For example, a person who is resident for tax purposes in Cameroon, who receives a local salary and dividends from a foreign company, is taxable in Cameroon on all of that income, including dividends received from abroad.

-

What is the operative event for the PIT?

The chargeable event is the event giving rise to the tax.

According to the provisions of Article 67 of the General Tax Code, each taxpayer is taxable on the basis of his actual income.

-

What is the maturity of the PIT?

Chargeability is defined as the right that the administration can claim at a given time from the taxpayer to obtain payment of tax.

Pursuant to the provisions of Article 68(1) of the General Tax Code, the PIT is payable when the income is made available to the taxpayer.

-

What are the reporting obligations of persons liable to tax at the PIT?

A tax obligation is the set of duties to which any natural or legal person is subject to the tax authorities.

In accordance with Article 74a of the General Tax Code, non-professional taxpayers receiving income are required to submit an annual summary income tax return by 30 June of each year.

-

How is the PIT paid?

Terms of payment are defined as the methods of payment, the maturity of payments or the payments to be made.

According to the provisions of Article 80 of the General Tax Code, the PIT is paid by instalments and deductions at source made during the year by the employer on each payment of the taxable amounts.

According to the provisions of Article L 7a of the General Tax Code, the method of payment of the taxes, duties and taxes of taxpayers submitted to the Summarized General Tax are bank transfers, electronic payments and cash payments exclusively at bank counters.

-

What is the payment term for the PIT?

The period for payment is the period allowed for the payment of the tax.

Pursuant to Article 82 of the General Tax Code, the PIT withheld at source must be remitted by the 15th of the following month to the tax revenue of the employer’s tax office.

-

What are the penalties for late payment of the PIT?

Tax penalties are the financial penalties (interest on late payments, fines and penalties) imposed by the administration for late payment of tax.

According to the provisions of Article L 106(1) of the General Tax Code, late payment of the PIT entails the application of late payment interest of 1.5% per month of delay, not exceeding 50%, and the application of a penalty of 10% per month of delay, not exceeding 30% of the tax due in principal.

-

Where to find out?

Get closer to your Tax Centre or visit the official website www.impots.cm, or call us using the number +237679735731 or +237698182555